How a company values its inventory directly impacts its profits, taxes, and financial statements.

FIFO (First In, First Out) and LIFO (Last In, First Out) are two of the most common methods used to calculate inventory costs, and they can result in very different financial outcomes-especially in industries affected by price fluctuations.

The method a company chooses affects how much it pays in taxes, how its profits appear on financial reports, and how well its inventory costs match reality.

FIFO frequently results in higher reported profits, whereas LIFO can decrease taxable income during periods of rising costs. The right choice depends on financial priorities, inventory flow, and market conditions.

In this article, we’ll break down how FIFO and LIFO work, their benefits and challenges, and how to calculate inventory costs using each method.

What is FIFO?

FIFO (First In, First Out) is an inventory valuation method that assumes the oldest inventory items are sold or used first, while the most recent purchases remain in stock.

The key idea behind FIFO is that inventory costs are recorded based on the earliest purchases, which means older, often lower-cost items are reflected in the Cost of Goods Sold (COGS). Conversely, newer, typically higher-cost inventory remains on the balance sheet.

This is particularly important in periods of rising prices, as FIFO results in lower COGS, higher net income, and a larger tax burden.

Since FIFO closely aligns with the physical movement of inventory, it is commonly used in retail, food production, and manufacturing. It ensures that older stock is sold before it expires, reducing the risk of spoilage, obsolescence, or product waste.

Advantages of Using FIFO

FIFO provides clear financial and operational advantages, making it a widely used inventory valuation method across different industries. From precise cost tracking to improved financial reporting, here’s why many companies prefer FIFO:

1. More Accurate Inventory Valuation

FIFO ensures that newer inventory remains on the balance sheet, which means reported inventory costs are closer to current market prices. This provides a more realistic financial snapshot, especially for businesses that need to assess the true value of their stock at any given time.

2. Higher Net Income in Inflationary Periods

When prices are rising, FIFO results in lower COGS because older, cheaper inventory is used for calculations.

This leads to higher reported profits, which can be beneficial for attracting investors or securing loans, as the business appears more profitable on financial statements.

3. Simpler and More Logical Inventory Flow

Since FIFO follows a natural inventory movement, it simplifies warehouse operations and aligns with real-world logistics.

This is particularly important for industries handling perishable goods, pharmaceuticals, and fast-moving consumer products, where selling older stock first prevents spoilage and obsolescence.

4. Globally Accepted Accounting Method

FIFO is permitted under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). This makes it the preferred option for international businesses, guaranteeing compliance with financial reporting regulations across the globe.

5. Lower Risk of Inventory Write-Offs

By continuously rotating stock and ensuring that older items are sold first, FIFO minimizes losses from expired or outdated inventory. Businesses managing products with limited shelf life or rapid technological advancements benefit significantly from this approach.

However, despite FIFO’s clear advantages, it may not always be the best fit. Pricing trends and tax strategies must be considered in conjunction.

Disadvantages of Using FIFO

While FIFO provides clear financial and operational advantages, it also presents drawbacks that may affect taxes, profitability, and the accuracy of financial reporting-particularly under certain market conditions. Here are some key disadvantages of using FIFO:

1. Higher Tax Liability in Inflationary Periods

When prices rise, FIFO results in lower COGS because older, cheaper inventory is used in calculations. This leads to higher taxable income, which can increase tax liability for businesses.

Companies looking to minimize taxes often prefer LIFO, which allows them to deduct the cost of newer, higher-priced inventory.

2. Less Reflective of Current Costs

FIFO bases COGS on older inventory costs, which may not accurately reflect the actual cost of replacing stock. During times of significant price fluctuations, financial reports may overestimate profitability, giving a misleading picture of actual margins.

This can be problematic for businesses that need up-to-date cost data for pricing and financial planning.

3. Not Always Ideal for Non-Perishable Goods

While FIFO works effectively for industries managing perishable goods, it might not be the most efficient method for businesses with durable or slow-moving inventory.

In sectors where older stock holds its value, FIFO might inflate reported profits and distort financial projections compared to methods like LIFO or weighted average cost.

4. Can Lead to Overstated Profits

During periods of inflation, FIFO produces higher net income since older, lower-cost inventory is used to calculate COGS. While this might seem like an advantage, it can create artificially high profit margins, making financial reports look stronger than they actually are.

This may lead to higher dividend payouts, misleading investors, and unrealistic financial expectations.

5. May Require More Inventory Tracking

FIFO assumes that older inventory is sold first, but in reality, businesses may not always follow this pattern.

Maintaining accurate FIFO records may require advanced inventory management systems to ensure the correct cost layers are applied. This can add complexity and administrative overhead to accounting and warehouse operations.

What is LIFO?

LIFO (Last In, First Out) is an inventory valuation method that assumes the most recently purchased inventory is sold or used first, while older stock remains in storage.

Unlike FIFO, which maintains a natural inventory flow, LIFO emphasizes the importance of newer, higher-cost inventory in cost calculations. This approach has a direct impact on a company’s financial statements and tax obligations.

The key characteristic of LIFO is that it aligns current costs with current revenues, meaning that in times of rising prices, the COGS will be higher, resulting in lower taxable income.

This offers a financial benefit, particularly for companies aiming to lower their tax burden during inflationary periods. However, adopting LIFO means that older inventory values stay on the balance sheet, which might not accurately represent the actual market value of a company’s stock.

Advantages of Using LIFO

LIFO offers specific financial and tax benefits, particularly for businesses dealing with fluctuating material costs and inflationary pricing. While it’s not as commonly used as FIFO, LIFO can provide strategic advantages in certain industries.

1. Lower Tax Liability in Inflationary Periods

When inventory costs are rising, LIFO records the most recent (higher-cost) inventory as an expense first, increasing the COGS. This results in lower taxable income, reducing the amount a company owes in taxes.

Businesses in oil, manufacturing, and construction often use LIFO to offset rising material costs and manage their tax burden.

2. Better Align of Costs to Revenue

Because LIFO expenses newer, higher-cost inventory first, it provides a more realistic view of current expenses. This method helps businesses align rising material costs with revenue from sales, giving a more accurate reflection of profitability during inflationary periods.

3. Financial Flexibility for Businesses with Volatile Costs

Companies that deal with rapidly changing raw material prices benefit from LIFO because it allows them to adjust COGS in response to market conditions. This flexibility benefits manufacturing industries such as metals, fuel, and construction materials, where price fluctuations impact profitability.

4. Potential Cash Flow Advantages

Since LIFO reduces net income in inflationary periods, businesses pay less in taxes, allowing them to retain more cash on hand for reinvestment in operations, inventory replenishment, or capital improvements.

Disadvantages of Using LIFO

While LIFO has tax advantages, it has several drawbacks that can impact financial reporting, compliance, and inventory management efficiency.

1. Not Permitted Under IFRS

LIFO is allowed under GAAP (Generally Accepted Accounting Principles) in the U.S., but it is not permitted under IFRS (International Financial Reporting Standards).

This means that businesses operating internationally cannot use LIFO in their financial reporting, limiting its practicality for global companies.

2. Inventory Valuation May Not Reflect True Costs

Under LIFO, older, lower-cost inventory remains on the balance sheet indefinitely, which may undervalue the true cost of remaining stock. This can be misleading, especially for companies that need accurate financial data for asset valuation, budgeting, and investor reporting.

3. Higher COGS Can Lead to Lower Reported Profits

While LIFO helps businesses reduce taxable income, it also means they report lower profits-which can be a disadvantage when seeking investors, bank loans, or business financing.

Financial institutions and stakeholders often prefer higher profit margins when evaluating a company's financial health.

4. More Complex Inventory Tracking and Management

Because LIFO does not follow the natural physical flow of inventory, it can make inventory tracking more complex. Businesses need strong inventory management systems to ensure accurate stock control, reorder points, and financial reporting.

Without proper oversight, LIFO can lead to inefficiencies in warehouse operations and difficulty managing stock rotation.

What Types of Companies Often Use LIFO?

LIFO is most commonly used by businesses dealing with non-perishable goods, fluctuating material costs, and industries where inventory costs are highly variable.

Since LIFO assigns the most recent (often highest-priced) inventory to the COGS, it helps companies reduce taxable income during periods of inflation.

However, because LIFO is not permitted under IFRS, it is primarily used by U.S.-based companies following GAAP accounting standards.

Here are the industries that benefit the most from LIFO:

1. Oil, Gas, and Energy Companies

Industries dealing with volatile commodity prices, such as oil and natural gas, often use LIFO to reflect the rising cost of raw materials in their financial statements.

By recording the most recent, higher-cost inventory as an expense first, these companies report higher COGS, which lowers taxable income and reduces tax burdens during inflationary periods.

2. Automotive and Heavy Equipment Manufacturers

Manufacturers of vehicles, machinery, and industrial equipment often experience fluctuations in material costs, such as steel and electronics.

LIFO allows these companies to account for rising production costs, ensuring that reported profits are not artificially inflated when raw materials become more expensive.

3. Retailers and Large Wholesalers

Big-box retailers, supermarkets, and wholesalers that keep large stocks of non-perishable goods sometimes utilize LIFO. This method helps counter increasing supplier costs by expensing the latest purchases first, which in turn lowers reported profits and tax obligations.

However, FIFO is still more common in retail due to its better inventory flow tracking.

4. Construction and Building Materials Suppliers

Companies in construction-related industries-such as lumber, concrete, and steel suppliers-often experience price volatility due to market conditions. LIFO allows these businesses to reflect current material costs in their COGS, helping to stabilize financial reporting.

5. Chemical and Pharmaceutical Industries

Some companies in the chemical and pharmaceutical sectors use LIFO to manage the impact of raw material price increases. While not common for perishable drugs, LIFO may be used for bulk chemicals and raw compounds where material costs fluctuate significantly.

What Types of Companies Often Use FIFO?

FIFO is the most commonly used inventory valuation method across industrial sectors where inventory needs to move in a natural order or where accuracy is a priority.

Since FIFO assumes that older inventory is sold first, it helps businesses maintain realistic financial reporting and ensures that stock doesn’t become obsolete or expire.

FIFO also generates higher reported profits during inflationary periods, which can be beneficial for attracting investors and securing financing.

Here are some of the industries that primarily use FIFO:

1. Food and Beverage Industry

Businesses dealing with perishable goods-such as grocery stores, restaurants, and food distributors-must ensure that older stock is sold before it expires.

FIFO helps minimize spoilage, waste, and quality issues, making it the standard choice for inventory management and financial reporting in the Food and Beverage sector.

2. Pharmaceutical and Healthcare Companies

FIFO is critical for companies handling medications, medical supplies, and healthcare products. These industries deal with expiration dates and regulatory requirements, making it essential to move inventory in a first-in, first-out manner.

3. Retail and E-Commerce Businesses

Clothing stores, electronics retailers, and online sellers often use FIFO to ensure newer, higher-priced inventory is accurately reflected in their financial statements. This method helps retailers:

- Avoid obsolete stock (e.g., last season’s fashion or outdated electronics).

- Provide a true representation of inventory costs for pricing and margin calculations.

- Maintain accurate profit reporting, especially when prices fluctuate seasonally.

4. Manufacturing Companies

Manufacturers rely on FIFO to track raw materials, work-in-progress (WIP), and finished goods. Using FIFO guarantees that older materials are used first, reducing the risk of stale inventory and aligning with production efficiency goals.

This is particularly useful in industries where materials can degrade over time or where costs increase significantly over production cycles.

5. Consumer Goods and Cosmetics Industry

Businesses selling packaged goods, personal care items, and beauty products often use FIFO to prevent stock from becoming obsolete or expiring.

This method ensures that products with shorter shelf lives-such as skincare, hair care, and hygiene products-move efficiently while maintaining accurate inventory valuation.

Why FIFO Is the Preferred Choice for Most Businesses

FIFO is generally easier to implement, aligns with the natural flow of inventory, and ensures financial statements accurately reflect true inventory costs. Unlike LIFO, FIFO:

- Provides a more realistic inventory valuation, preventing outdated costs from lingering on the balance sheet.

- It is permitted under IFRS, making it suitable for global businesses.

- Ensures that perishable and time-sensitive goods don’t go to waste.

How to Calculate FIFO and LIFO

Understanding how to calculate inventory costs using FIFO and LIFO is essential for accurate financial reporting and inventory management.

Each method follows a different approach to determining the Cost of Goods Sold (COGS) and ending inventory value, which directly impacts a company’s profitability, tax liabilities, and balance sheet accuracy.

Below, we’ll break down the formulas for FIFO and LIFO, along with how to calculate the value of the remaining inventory under each method.

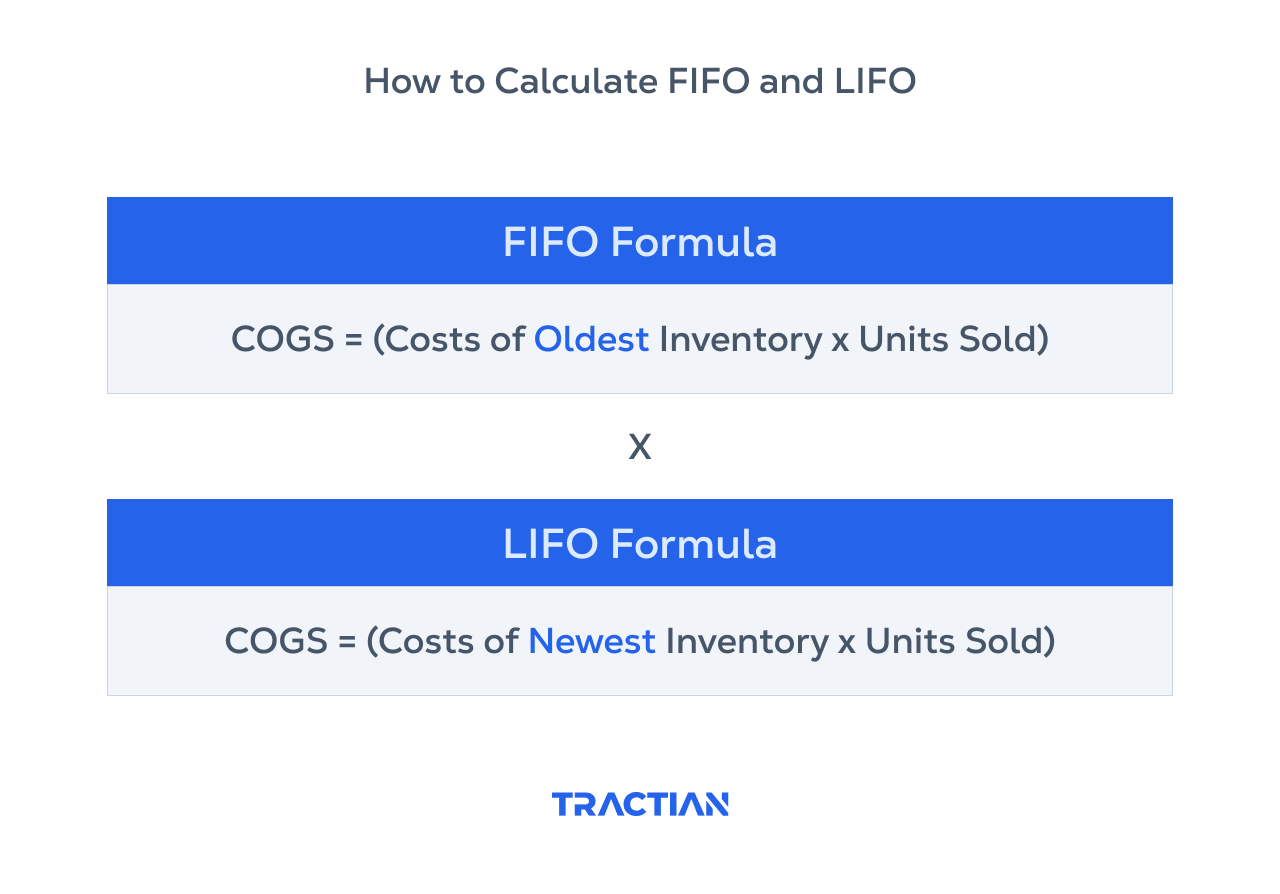

FIFO Formula

FIFO (First In, First Out) assumes that the oldest inventory is sold first, meaning that the cost of goods sold (COGS) is based on the earliest purchase prices, while the most recently purchased inventory remains in stock.

Example Calculation

A company purchases:

- 100 units at $10 each in January

- 100 units at $12 each in March

- 100 units at $14 each in June

If 200 units are sold, FIFO assumes the first 100 units at $10 and the next 100 units at $12 are used for COGS:

The remaining 100 units at $14 each stay in inventory.

LIFO Formula

LIFO (Last In, First Out) assumes that the newest inventory is sold first, meaning that the latest purchase prices are assigned to COGS, while the older inventory remains on the balance sheet.

Example Calculation

Using the same purchase data as before:

- 100 units at $10 each (January)

- 100 units at $12 each (March)

- 100 units at $14 each (June)

If 200 units are sold, LIFO assumes the 100 units at $14 and 100 units at $12 are used for COGS:

The remaining 100 units at $10 each stay in inventory.

Key Differences in Calculation

- FIFO results in lower COGS and higher ending inventory value during inflation.

- LIFO results in higher COGS and lower ending inventory value, reducing taxable income.

- FIFO is better for financial reporting accuracy, while LIFO provides tax advantages.

FIFO and LIFO: Choosing the Right Method for Industrial Operations

For industries that rely on heavy equipment, spare parts management, and asset-intensive operations, inventory valuation directly impacts maintenance efficiency, cost control, and uptime reliability.

The choice between FIFO or LIFO influences everything from how spare parts are used to how financial resources are allocated for repairs and replacements.

This difference of influence between FIFO and LIFO is why aligning your maintenance strategy with your inventory is so important.

Which Method Works Best for Industrial Maintenance?

For asset-heavy industries, FIFO is often the better fit because:

- It ensures that older inventory is used before newer stock, preventing waste.

- It provides an accurate financial picture, helping with long-term maintenance planning.

- It aligns with real-world spare parts usage, keeping operations predictable.

LIFO, while useful for managing tax liabilities, doesn’t always reflect true maintenance costs. If a company is stocking critical spare parts, using LIFO can result in an outdated inventory valuation, creating discrepancies between financial records and actual asset conditions.

A CMMS (Computerized Maintenance Management System) helps industrial teams track inventory in real-time, ensuring that maintenance decisions align with inventory strategies-whether using FIFO, LIFO, or a hybrid approach.

How To Improve Your Inventory Valuation with Tractian’s CMMS

FIFO prioritizes older inventory, keeping spare parts fresh and preventing waste, while LIFO helps businesses manage rising costs by expensing the newest inventory first.

Regardless of which method a company uses, poor inventory tracking leads to stock shortages, excess parts sitting unused, and maintenance teams scrambling for replacements when equipment fails.

Without a clear system in place, even the best valuation method fails to deliver efficiency where it matters most-on the plant floor.

Tractian's CMMS eliminates the guesswork by providing real-time visibility into stock levels, part usage, and reorder points. Instead of overordering materials that collect dust or running out of critical components at the worst possible time, maintenance teams always know what’s in stock, what’s needed, and when to restock.

Beyond just tracking, intelligent inventory management simplifies maintenance workflows. Tractian can help you improve your industry's results with less downtime, fewer costs, and a maintenance team that works smarter, not harder.

Optimize your inventory tracking and keep your maintenance operations running smoothly. See how Tractian's CMMS can elevate your industry to the next level.